Following the announcement of a stamp duty holiday in England on property purchases up to £500,000, the Scottish Government raised the nil LBTT threshold from £145,000 to £250,000 on 15th July 2020.

This means that anyone buying a property in Scotland up to the value of £250,000 will not pay any LBTT.

This will be in place until 31st March 2021. The Scottish Government still need to approve it within Parliament, but this is expected to take place within the required 28-day legislative period.

In this article, EPPG will answer commonly asked questions this week about LBTT and discuss what this change means for Scottish purchasers.

What is LBTT?

Land and Building Transaction Tax (“LBTT”) is Scotland’s version of stamp duty. It is a property tax applied to the purchase of residential and commercial property in Scotland.

All EPPG firms will advise you how much LBTT is payable for your purchase along with other fees and outlays at the outset.

How much is LBTT in Scotland now?

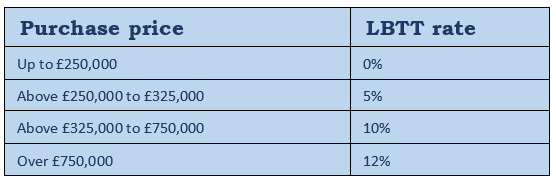

For residential property transactions, the rate of tax payable is determined by reference to the amount of the chargeable consideration for the transaction falling within the bands below.

The LBTT rates and bands for residential transactions were changed on a time limited basis with effect from 15 July 2020.

The following LBTT rates apply for residential transactions with an effective date of 15 July 2020 to 31 March 2021:

How much LBTT will I save with these changes?

The holiday means that anyone purchasing a property under £250,000 will not have to pay any LBTT, unless it is a second home in which case the 4% Additional Dwelling Supplement (ADS) applies.

If you are purchasing a property over £250,000, then you will only pay LBTT on the amount over £250,000 according to the thresholds and bands outlined above. Raising the 0% threshold from £145,000 to £250,000 means people purchasing a property over £250,000 will save £2,100 on LBTT, even if you are liable for ADS.

I’m currently in the process of buying a property, what happens next?

If your transaction is due to settle between 15th July 2020 and 31st March 2021 inclusive, then you will benefit from the new rates. If you have had an Offer accepted or concluded missives but have not yet settled, you will benefit.

I’m a first-time buyer – what does this mean for me?

First time buyers in Scotland used to pay no LBTT on first time purchases up to £175,000 as opposed to £145,000. This meant they could save an additional £600 compared to non-first-time buyers.

Now, like all other buyers, first time buyers will benefit from no LBTT on a purchase up to £250,000.

In addition to the changes to LBTT, the Scottish Cabinet Secretary for Finance also announced investing an additional £50 million into the popular Scottish First Home Fund Scheme. Successful applicants to this scheme could get a grant of up to £25,000 towards their first property purchase. EPPG covered this scheme in this article here along with details on other first time buyer schemes available in 2020.

I am planning on buying a second home – are there any changes to ADS?

The Additional Dwelling Supplement (ADS) is a 4% surcharge which applies to second home purchases. This charge still applies on transactions moving forward, but you will still benefit from the LBTT saving.

If you are planning to sell your main property you can claim the ADS amount back provided you sell within 36 months, up from the previous 18 month deadline. Following a request from the Scottish Law Agents Society to Revenue Scotland to extend the period that you can reclaim ADS tax the Scottish Government have confirmed that the period has been extended to 36 months. This extension of 18 months will allow sellers 36 months in total from the date they purchased their additional property to reclaim a refund of the ADS tax paid.

How does this compare to England and Northern Ireland’s stamp duty changes, introduced by Westminster?

If you are buying a property in England or Northern Ireland between now and 31st March 2021, you will not pay any stamp duty on property purchases up to £500,000 so there is lot of differences with this compared to the Scottish Government’s approach.

If you are buying a property higher than £500,000 in England and Northern Ireland, the amount of stamp duty also varies considerably to Scotland.

In addition, investors in Scotland who are liable for ADS will have to pay a lot more compared to English and Northern Irish counterparts.

Examples:

EPPG believe that the reduction in LBTT announced in Scotland is welcome news, but an extension of the 0% rate of LBTT from £145,000 to £325,000 would have helped even more buyers particularly those in Edinburgh where the average selling price exceeds £250,000.

This would have resulted in 90% of buyers not paying any LBTT between now and 31st March 2020.

The LBTT holiday in Scotland is most certainly welcome news, but many buyers in Scotland will be discontent when comparing to the relief available to buyers in England and Northern Ireland.

To discuss further, or if you are looking to budget for your prospective purchase, get in touch today for a free no obligation and transparent quotation from an EPPG firm.